If you’re thinking of making a serious game or educational experience, you need to understand the unit economics to see if it’s financially feasible to build it. Unit economics is a tool that will help you answer three basic questions about any opportunity:

- What is my breakeven?

- What is my pre-tax cash flow?

- How long until payout?

We’ll explain what each of these questions means, and why each is important, later in this article. For now, understand that these are three main financial questions you’ll need to answer when analyzing entrepreneurial opportunities, whether you’re launching a whole new business, investing in a venture or project, or simply creating a new product for your current organization.

Unit economics also prevents you from improperly categorizing or combining variable costs, fixed period costs, and primary sunk investments, allowing you to budget for the project or venture more accurately. Lastly, if you build a simple spreadsheet that performs the calculations for you, you can do a sensitivity analysis, changing assumptions until you’ve identified the best business model for proceeding. Don’t worry—the formulas are quite simple, even though few entrepreneurs and managers know how to do them. We’ll work through a simplified case study to illustrate the critical elements of unit economics.

Unit economics always matter

Even if you’re not a for-profit business looking to make money from your game, the unit economics are still important to calculate. Budgets still matter, no matter what kind of organization you are. I guarantee that, at minimum, someone at the top of your organization very much cares how much your game will cost to make, how much it will increase overhead, how much revenue it can bring in, and so on. I’ll write this article assuming that you plan to sell your own game or experience for a profit, but the same rules of unit economics apply to any kind of organization. Even if you’re only building the experience for internal use within your own organization, some sort of value is likely to change hands from department to department, even if only at the accounting level. Further, you can still calculate the unit economics formulas even if you set the price to $0.

Also, many successful software companies got their start as a spin-off from a larger corporation or government entity. As in, the parent company or agency develops the software for its own internal uses, then realizes other companies could benefit from the same software, and so decides to sell licenses to outside parties to generate a new revenue stream. If you develop highly valuable games for your organization’s internal use, don’t be surprised if you’re suddenly the head of a division selling your games to the open market. If you do your unit economics now, you’ll be better prepared if and when you find yourself in that situation.

Now you know why to calculate unit economics, so let’s set up our fictional but realistic case study.

Case study

Let’s say you were a technical trainer working for a large corporation. You decided you wanted to make a game that teaches a skill that’s fundamental to the work completed by many of your company’s employees. You also realized that a game that teaches this particular skill would be valuable to companies and workers outside your organization, too.

You pitched your manager on the idea that you’ll build the game and sell it on the open market as an additional revenue stream for the company. She asked you how much the game would cost to build, how many copies of the game you would have to sell to cover costs each month, how much money it’s likely to make, and how long before the company recouped its invested capital. Fortunately, you had already calculated the unit economics, so you had the answers ready. The numbers made sense, you sounded confident and organized, and so she agreed. She allocated a small budget your way, and you were off to the races.

After some initial planning and organization, you hired five contract game developers and designers to help you build the game. The salaries for the six of you totaled about $40,000 per month, and it took you four months to build the game. Once the game was finished, you let most of the team go. You retained two full-time employees plus yourself to fix bugs, take customer service calls, market and sell the game, and handle any other tasks. Your combined salaries cost only $20,000 per month moving forward. You also spent $5,000 to build a website and $15,000 on marketing your game for launch. Game licenses (GLs) are priced at $20 each, meaning that each person who buys your game pays you $20.

The game was a success. Your company loved it, and you were promoted to VP of the company’s newest division: training and development software. Further, the game did fairly well outside the company. Almost immediately, sales reached 2,500 units (i.e., unique game licenses and downloads) each month. You’re already planning what games to build next.

Amazingly, all the revenues, costs, and cash flows turned out exactly as you predicted in your original unit economics calculations. Let’s take a closer look.

Assumptions

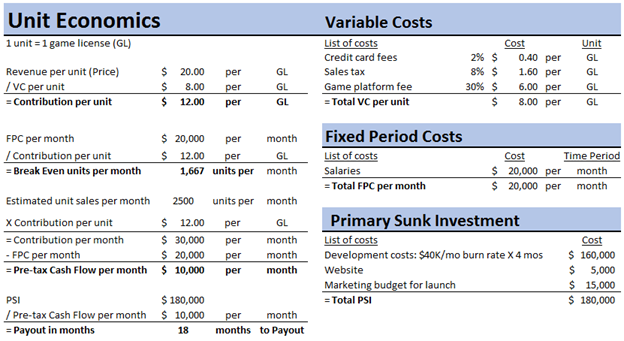

Unit economics uses several assumptions (aka variables) in the formulas. These assumptions include units, price, three types of costs, and unit sales. Figure 1 shows all the assumptions and formula calculations as described in our case study. Throughout the rest of this article, we’ll reference this figure one section at a time.

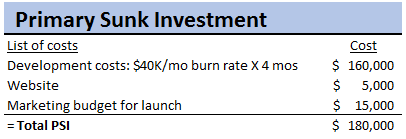

Figure 1: Case study assumptions and formula calculations

Units

A unit (i.e., a single unit sold) can be many different things, but for our purposes, a unit will be one GL or download of your game. Every time a person, company, school, etc., buys and downloads a single copy of your game, that’s one unit. If someone buys two licenses for two different computers or devices, then that counts as two units. If you’re a pizza restaurant, a unit is probably going to be a single pizza. If you’re a T-shirt company, a unit will be a single T-shirt. In your venture, a unit is a single game license.

Price

Price is what you’ll charge to sell one unit. Game prices vary greatly. However, for the purposes of this case study, you’re charging $20 per GL.

![]()

Costs

Unit economics requires you to differentiate between three different kinds of costs: variable costs per unit (VC), overhead or fixed period costs per month (FPC), and primary sunk investment (PSI). It’s very important that you categorize costs correctly. For example, if you list an FPC, such as an employee’s salary, under VC or PSI, then your monthly budget will be way off, as will your VC or PSI.

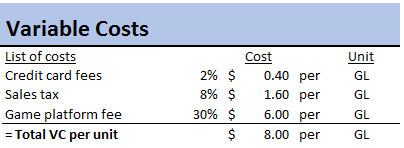

Variable costs per unit

VC are costs that you incur each time you sell a single unit of your game. These typically include:

- The cost of the raw materials required to make one unit

- Sales commissions

- Credit card fees

- Sales taxes

- Delivery costs

VC can be a percentage of the price or a set dollar amount per unit. When adding up the VC, make sure to convert any percentages to an actual dollar amount so all VC can be added together.

In the case of a game that’s downloaded via the Internet, your VC will typically be limited to:

- Credit card fees of about 2% – 3% of the unit price

- Sales taxes, varying depending on your location but generally around 7% – 8% of the unit price

- Any fees (aka revenue splits) charged by the platform or marketplace that markets and distributes your game, often around 30% of the unit price (this is what Steam is purported to charge)

The total VC for your game will thus be 40% of the price. If you charge $20 for your game, the VC will be $8/unit. If you sell one unit in a given month, you incur the $8 just once that month. If you sell two units, you incur the $8 twice, totaling $16 in VC for that month. If you sell 1,000 units in a month, you’ll incur $8,000 in VC that month.

Note: Always include the full label or mathematical units (e.g., %, $, per unit, per month) for every number used in unit economics so you don’t mistakenly add two numbers together with different mathematical units or labels.

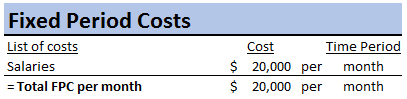

Fixed period costs per month

FPC (aka overhead) are costs that you incur each month no matter what, such as:

- Salaries

- Rent

- Insurance

- Utilities

If you sell zero units in a given month, you still have to pay your employees’ salaries and the rent payment. The landlord doesn’t care how many units you sell, as long as you keep paying rent on time. However, if you sell 1,000 units, your employee salaries and rent payments stay the same.

For the purposes of this case study, we’ll assume your only FPC will be salaries because your rent, insurance, utilities, and other overhead costs will already be covered by the other business activities of your parent company. An accountant could certainly allocate some of these other costs to this project, but realistically, the business will go on whether your game is successful or not. Further, your small team is not likely to increase rent, insurance, or utilities by launching your game either. Therefore, salaries will be our only FPC.

The number of full-time employees you’ll need depends on the scope and complexity of your game and the speed at which you’re going to develop it. A team of two or three people can build and launch a very simple game perhaps within a few months, maybe as long as a year. A team of 15 developers can launch a larger and more complex game in 6 – 12 months. Major game development companies require hundreds of people to launch each big-budget title over the course of a year, or sometimes over several years. As mentioned above, you decided to hire five people plus yourself, and it took you four months to build the game.

However, once the game was built, you didn’t need all those people anymore, just the small crew of two full-time employees plus yourself. The larger original team of five developers was an up-front cost that you only incurred one time to build the game. Thus, that team won’t be considered an FPC. Only the new, smaller team that’s staying on indefinitely will be considered an FPC.

Primary sunk investment

PSI are costs that you incur one time at the very beginning of a venture. These costs are required to get the business and product launched. These often include:

- Development costs

- Signs, logos, and other branding

- Website and app

- Office or location build-out

- Equipment

- Operating losses incurred until the product is launched and breakeven is reached

Just like with some of the variable and fixed period costs, many of these PSI will not apply to your serious game development project. For example, in our case study, you already had all the computers and equipment you needed.

The biggest PSI to consider here is the original team of developers. This team costs $40,000 per month, and it took you four months to build the game. $40,000 X 4 months = $160,000. Add in the $5,000 you spent for the website and the $15,000 for marketing the launch, and that puts your PSI at $180,000.

Unit sales

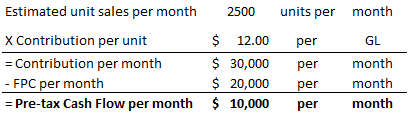

The final assumption or variable in unit economics equations is unit sales. How many units do you estimate you’ll realistically be able to sell each month? I can’t answer that for you, because it depends on the size of your market, the demand for your particular game, how good your game is, how heavily you market and promote the game, how much competition it has, any partnerships or business development you have lined up, a little bit of luck, and so on. In our case study, however, you sold 2,500 units per month.

![]()

Formulas and analysis

Now that we’ve decided values for all our variables or assumptions, we can calculate the unit economics formulas. The four formulas are as follows:

- Contribution = price – variable costs

- Breakeven = fixed period costs / contribution

- Pre-tax cash flow = contribution X unit sales – fixed period costs

- Payout = primary sunk investment / pre-tax cash flow

Let’s walk through each of them, in order, using the assumptions in our case study.

Contribution

Contribution per unit (aka contribution or gross profit per unit) is how much each new unit sale contributes to the company. Knowing the contribution per unit is somewhat useful in its own right, but its biggest importance comes from its role in the remaining three formulas that are calculated after calculating contribution.

The higher the contribution, the better, because you want to make as much profit on each sale as possible. In our case study, the contribution is:

Breakeven

Your breakeven is the number of unit sales you need to sell each month in order to pay for all your FPC. If you sell fewer units than that each month, the company loses money. If you sell exactly the number of units needed to break even each month, the company neither loses nor profits. If you sell more units than that, the company makes a profit. Obviously, knowing how many units you need to sell to break even is critically important to any entrepreneur, executive, or manager.

The lower the breakeven is, the better, because that reduces the risk of losing money each month. In our case study, the breakeven is:

Pre-tax cash flow

Pre-tax cash flow is exactly what it sounds like: how much money the company will make before paying taxes. This is roughly analogous to EBITDA (earnings before interest, taxes, depreciation, and amortization) on an income statement. Obviously, being able to estimate how much monthly cash flow a new product is likely to create is also critically important to entrepreneurs, executives, and managers.

The higher the pre-tax cash flow, the better, because we all want to make more money. In our case study, the pre-tax cash flow is:

Payout

Payout is how many months (or years) it will take for the venture to earn enough pre-tax cash flow to pay back the full amount of capital invested to build and launch the project.

The sooner the payout, the better, because it’s less risky to get any invested capital back as quickly as possible. In our case study, the payout will be:

Sensitivity analysis

While the assumptions above are fairly realistic for many small game-development projects, your actual assumptions may be quite different. That’s OK. Similarly, you may not even know what your price, costs, and unit sales will be yet. That’s OK, too. Just build a spreadsheet that calculates the formulas above. Make sure you can easily change any of the variables. Then put your own numbers in and see how the results change. Make a note of the results. Then change one or more of the assumptions, and make a note of those results. Do this again and again until you have a deep understanding of how even small changes to any of the variables—whether the price, VC, FPC, PSI, or unit sales—will impact your breakeven, pre-tax cash flow, and payout.

Don’t just make up numbers, however. Instead, do your homework. You must research as best you can what your costs will likely be, what price point you can likely sell at, and how many units you can realistically sell at that price point. If you can’t find any information on these assumptions, you’ll have to make educated guesses, but the better the information you feed into the unit economics formulas, the more accurately they’ll predict breakeven, pre-tax cash flow, and payout.

Once you’ve tested out every realistic scenario in your spreadsheet, and not a moment before, you will finally be well enough informed to decide whether the project is even worth doing, or whether it’s too small or too risky to proceed.

Note that unit economics analyses are highly subjective. While some opportunities are clearly bad—perhaps because the contribution margin is close to zero, they have a negative pre-tax cash flow, they’ll never reach breakeven, or payout is absurdly far in the future—the analyses of other opportunities are less clear. For example, take our case study’s calculations of:

- $12 contribution per GL

- 60% contribution margin (i.e., $12 contribution from $20 price)

- A breakeven of 1,667 GL per month

- $10,000 pre-tax cash flow per month

- An 18-month payout

Are they good or bad? Risky or safe? Is this opportunity worth pursuing or not? Frustratingly, the answer to all these questions is, “It depends.” It depends on your (or your organization’s) balance sheet, liquidity, current profitability, operational focus, strategic plan, competition, market trends, and more. The same opportunity and unit economics might be a perfect investment for one company and a disaster for the next.

Only you and your team can decide what these numbers mean in the context of your own company and circumstances. That said, you’ll make far better decisions about whether to proceed with this or any opportunity if you have the unit economics numbers in front of you than if you don’t.

Summary

After you’ve built the spreadsheet—and it should only take you five minutes if you’re proficient in Microsoft Excel, Apple Numbers, Google Sheets, or other spreadsheet programs—then you can use it to analyze the viability of any new opportunity, no matter what the product or service.

For example, what if you’re considering building game-based eLearning experiences for big corporate clients? No problem. Just use your unit economics spreadsheet. Your unit could be selling, building, and delivering one training game to one client. Your VC will be way higher, but so will the price. The number of units sold will be way smaller. FPC and PSI could be high or low, depending on the size of your team and how much you spend before closing your first deal.

The unit economics will look very different for every single opportunity, but the formulas will work just the same, and the results will always be incredibly informative and useful.

Additional resources

You can find several in-depth articles about unit economics on my blog. If you email me, I’ll happily send you a unit economics spreadsheet template at no cost.